Circular 96/2026/TT-BTC amend Circular 67/2023/TT-BTC guiding the Law on Insurance Business and Decree 46/2023/ND-CP

- Summary

- Content

- Status

- Vietnamese

- Related documents

- Diagram

- Download

Please log in to your Advanced Package to view the full text. Do not have an account yet? Register here.

Please log in to use this function

Please log in to use this function

ATTRIBUTE

| Issuing body: | Ministry of Finance | Effective date: | Known Please log in to a subscriber account to use this function. Don’t have an account? Register here |

| Official number: | 96/2026/TT-BTC | Signer: | Le Tan Can |

| Type: | Circular | Expiry date: | Updating |

| Issuing date: | 02/07/2026 | Effect status: | Known Please log in to a subscriber account to use this function. Don’t have an account? Register here |

| Fields: | Enterprise, Insurance |

The Effect status of this document is known.This feature is available to Advanced account holders. Please log in to a subscriber account to view Effect status. Don’t have an account? Register here

THE MINISTRY OF FINANCE

No. 96/2026/TT-BTC | THE SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, July 02, 2026 |

CIRCULAR

Amending and supplementing a number of articles of the Minister of Finance's Circular No. 67/2023/TT-BTC dated November 02, 2023, guiding a number of articles of the Law on Insurance Business and the Government’s Decree No. 46/2023/ND-CP dated July 01, 2023, detailing the implementation of a number of articles of the Law on Insurance Business

Pursuant to the Law No. 08/2022/QH15 on Insurance Business, which was amended and supplemented by the Law No. 139/2025/QH15 (hereinafter referred to as Law on Insurance Business);

Pursuant to the Government’s Decree No. 46/2023/ND-CP detailing the implementation of a number of articles of the Law on Insurance Business, which was amended and supplemented by the Decree No. 97/2026/ND-CP;

Pursuant to the Government’s Decree No. 29/2025/ND-CP, defining the functions, tasks, powers and organizational structure of the Ministry of Finance, which was amended and supplemented by the Decree No. 166/2025/ND-CP;

At the proposal of the Director of the Insurance Supervisory Authority;

The Minister of Finance promulgates the Circular amending and supplementing a number of articles of the Minister of Finance's Circular No. 67/2023/TT-BTC dated November 02, 2023, guiding a number of articles of the Law on Insurance Business and the Government’s Decree No. 46/2023/ND-CP dated July 01, 2023, detailing the implementation of a number of articles of the Law on Insurance Business.

Article 1. Amending and supplementing Clause 2 Article 1 as follows:

“2. The Circular guides Point b Clause 2 Article 119 of the Law on Insurance Business regarding regularly disclosed information and Clause 6 Article 7, Point c Clause 2 Article 32, Article 44, Clause 7 Article 49, and Points k and p Clause 3 Article 50 of the Government’s Decree No. 46/2023/ND-CP dated July 1, 2023, detailing the implementation of a number of articles of the Law on Insurance Business, amended and supplemented by the Decree No. 97/2026/ND-CP (hereinafter referred to as Decree No. 46/2023/ND-CP), including information templates for the insurance business database; templates of explanatory documents for the rate-making methodology and considerations; guidelines and illustrations for technical reserving methods, formulas, and considerations; the time of recognizing insurance revenue for each type of insurance; and management of individual insurance agents, support payments, and remuneration payments.”.

Article 2. Amending and supplementing the first paragraph and a number of clauses of Article 7 as follows:

1. To amend and supplement the first paragraph of Clause 1 Article 7 and Clause 1 Article 7 as follows:

Any insurer/foreign non-life insurer’s branch/mutual organization providing microinsurance/insurance broker/insurance agent that provides insurance services and products online must satisfy the requirements in terms of services, technology, confidentiality and data retention as specified in the law regulations on e-transactions, data, cybersecurity, and e-commerce, as well as shall:

1. Formulate and issue its internal regulations stipulating the distribution of insurance services and products online, which include the following main information: description of the processes of transaction; control of risk and ensuring of cybersecurity; and the rights and obligations of related parties; complaint/dispute settlement mechanisms; personal data protection policies; incident response plans and backup systems; data retention and measures for handling acts of non-compliance with the internal regulations.”.

2. To amend and supplement Clause 7 Article 7 as follows:

“7. Classify and take measures to secure the respective information system as specified in the law regulations on cybersecurity and security of information systems by classification and electronic transactions in financial activities.”.

Article 3. Amending and supplementing Clause 2 Article 17 as follows:

“2. In addition to satisfying the requirements specified in Clause 1 of this Article, investment-linked insurance policies and pension policies must also explicitly indicate how insurance premiums and fees/charges levied on the policyholder are allocated. The charges/fees levied on the policyholder must be consistent with Article 99 of Decree 46/2023/ND-CP. In case of adjusting the charges/fees levied on the policyholder, the insurer shall notify the policyholder in writting within at least 03 months before the new charges/fees are applicable.”.

Article 4. Amending and supplementing Points a and b Clause 1 Article 20 as follows:

“a) Calculate insurance rates and engage in the formulation of the terms and conditions of insurance/ reinsurance products; confirm that premiums and charges/fees levied on the policyholders (for investment-linked insurance and pension products) are determined based on statistical data, guarantee the economic and technical feasibility of the products, fairness to policyholders, compliance with the law regulations, the solvency of the insurer/ reinsurer/ Vietnam-based foreign branch; carry out annual review and assessment of actuarial assumptions to ensure that the use of such actuarial assumptions are reasonable, consistent, and appropriate to the statistical data and the actual statistical data of the enterprise or branch; and promptly propose adjustments or changes to the actuarial assumptions to the General Director (Director) of the insurer/ foreign non-life insurer’s branch where necessary.

b) Calculate and ensure adequate operational provisions as required by the law regulations;”.

Article 5. Amending and supplementing a number of points of Clause 22 as follows:

1. To amend and supplement Point a Clause 1 as follows:

“a) The insurer/ foreign non-life insurer’s branch may use the death probability sourced from any of the following:

- 1980 CSO Mortality Table specified in Appendix V issued together with this Circular; other probability factors based on this 1980 CSO Mortality Tables;

- Mortality tables developed on the statistical data collected by the insurer/ foreign non-life insurer’s branch in at least 10 years of bona fide product distribution;

- Mortality tables provided by the holding company of the insurer/ foreign non-life insurer’s branch or by the reinsurer, organization accepting inward reinsurance;

If the death probability used by the insurer/ foreign non-life insurer’s branch is 70% higher than that of the 1980 CSO Mortality Table, such insurer or foreign non-life insurer’s branch must explain the reasonableness thereof and the characteristics of the customer category to which such higher rate is expected to be applicable.”.

2. To amend and supplement Point a Clause 2 as follows:

a) Assumptions about expenses for providing the insurance product (fixed expenses and variable expenses), which shall be determined based on the statistical data of the 3 consecutive years immediately preceding the year in which the application dossier is submitted and business plans of the insurer/foreign non-life insurer’s branch. In case an insurer/ foreign non-life insurer’s branch has been in operation for less than 3 years, the assumptions regarding the expenses for providing the insurance product shall be determined based on its 5-year business plan;”.

3. To amend and supplement Point c Clause 3 as follows:

“c) The cost of insurance for investment-linked insurance products and pension products shall comply with the following provisions:

- For investment-linked insurance products and pension products providing the death benefit and the total permanent disability benefit: the cost of insurance shall not exceed 80% of the probability of dying in the 1980 CSO Mortality Table set out in Appendix V issued together with this Circular, multiplied by the sum assured.

- For investment-linked insurance products providing only the death benefit: the cost of insurance shall not exceed 72% of the probability of dying in the 1980 CSO Mortality Table set out in Appendix V issued together with this Circular, multiplied by the sum assured.

In cases where an insurer applies a cost of insurance higher than 80% of the limits specified above, it must explain the reasonableness thereof and characteristics of the customer category to which such higher cost of insurance shall be applicable;”.

Article 6. Amending and supplementing a number of points of Clause 25 as follows:

1. To amend and supplement Point d Clause 1 as follows:

d) Specific cases and considerations for premium increase or reduction shall be notified.

The increase in premium must be based on factors that increase the covered risks.

If the insurance premium is reduced, in any case, the reduced premium shall not be lower than the pure premium and shall be based on any or many of the factors that may reduce, spread or share the risks or reduce the operating expenses, including the quantity of insured vehicles, the excess or deductible selected, the claims history, the product distribution channel, and other factors (if any). In the case where the premium is reduced due to direct distribution, the maximum reduction shall not exceed the commission as specified in Article 51 of this Circular;”.

2. To amend and supplement Points a and b, Clause 2 as follows:

“a) The pure premium shall be determined based on the statistical data collected by the non-life insurer/foreign non-life insurer’s branch with the scalability and continuity in a time series of at least 5 consecutive years.

In cases where the statistical data does not ensure the scalability and continuity, the non-life insurer/foreign non-life insurer’s branch may:

- Use the pure premium announced by the competent authority/organization;

- Determine the pure premium based on the statistical data, the official and public data disclosed or published by organizations lawfully established and operating in Vietnam;

- Use the pure premium provided by the holding company, or any reinsurer/foreign insurance organization accepting outward reinsurance which must be rated at least “BBB” by the Standards & Poor’s or Fitch Ratings, “B++” by A.M. Best, “Baal” by Moody’s or otherwise equally rated by another accredited rating agency in the fiscal year nearest to the time the application dossier for registration of its rate-making methodology and considerations is submitted, and have experience in reinsurance of this type of risk in Vietnam or Asia. In case of adjusting (increasing or decreasing) the pure premium provided by the foreign reinsurer, the insurer/foreign non-life insurer’s branch must give reasons therefor. Pure premium provided by any reinsurer/foreign insurance organization accepting inward reinsurance must be used in line with the insurance benefits that the insurer/foreign non-life insurer’s branch expects to provide under the terms and conditions of the insurance product.

In case an insurer/foreign non-life insurer’s branch determines the pure premium for insurance risks applicable to environmentally friendly motor vehicles and motor vehicles using motor vehicles utilizing clean energy, green energy, and environmentally friendly technologies in accordance with Circular No. 53/2024/TT-BGTVT dated November 15, 2024, or any amending or supplementing documents (if any): The insurer/ foreign non-life insurer’s branch may use statistical data sources publicly published by domestic and international organizations on their official websites or use such statistical data in combination with the statistical data of the enterprise or branch covering a minimum period of 3 consecutive years.

The use of the product implementation data sources specified at this Point, the risk assessment process, and the product discontinuation and product re-pricing process shall be clearly specified in the internal processes for product development and rate-making. This internal processes must be approved by the Board of Directors (Members' Council) or the General Director (Director). The compliance with the internal processes for product development and rate-making must be reviewed annually by the internal audit.

b) The pure premium shall be specifically determined for each peril or for some of the following perils: vehicular crash and collision (including collision with other objects); overturning, rollover, submersion, falling; falling objects; fire and explosion; natural disasters; theft; and other perils (if any).

Upon notifying the application of, or any change to, the rate-making methodology and considerations for motor insurance, the insurer/ foreign insurer's branch shall not change the notified pure premium for at least the subsequent 12 months with respect to the same type of motor vehicle, purpose of business and use of the motor vehicle, year of manufacture of the motor vehicle, and customer category.”.

Article 7. Amending and supplementing the first bullet point of Point b Clause 2 Article 38 as follows:

“- 80% of the 1980 CSO 1980 Mortality Table and other technical considerations, which shall be consistent with the insurance benefits that the insurer commits to the customers in the insurance product terms and conditions.

In any case, the mortality and probability factors used for reserving must not be lower than those used by the insurers for rate-making.”.

Article 8. Amending and supplementing Clause 3 Article 40 as follows:

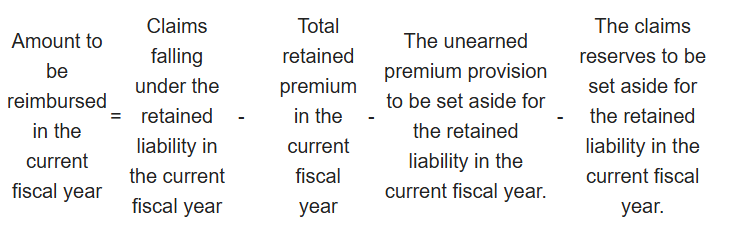

“3. For any non-life insurer/ Vietnam-based branch of a foreign non-life insurer, or reinsurers providing health insurance, term life insurance with the coverage period of 01 year or less. The amount to be set aside annually shall comply with Point b, Clause 1, Article 37 of this Circular. This reserve is used to pay claims when catastrophic events occur and the total retained premium collected in a fiscal year, after accounting for the unearned premium provision and outstanding claims reserve, is not sufficient to cover the payment of claims for the retained liability of the non-life insurer/Vietnam-based foreign branch/reinsurer.

The maximum amount to be reimbursed from this reserve is calculated using the following formula:

Article 9. Amending and supplementing the title of Section 4 of Chapter IV as follows:

“REVENUES AND EXPENSES”

Article 10. Amending and supplementing Clause 1 Article 41 as follows:

“1. Any insurer/any Vietnam-based branch of any foreign non-life insurer shall record the direct insurance premiums into the insurance business revenue account upon the inception of insurance coverage for the policyholder, specifically as follows:

b) In case the insurance policy has been concluded and the policyholder has fully paid the premium;

b) There is evidence indicating that the insurance policy has been concluded and the policyholder has fully paid the premium;

c) When the insurance policy has been concluded and the non-life insurer/foreign non-life insurer’s branch has agreed with the policyholder on the insurance premium payment term as specified at Points a and c, Clause 2, Article 26 of this Circular, the non-life insurer/ foreign non-life insurer’s branch shall record into its revenue the insurance premiums payable by the policyholder as agreed in the insurance policy account when the insurance term starts;

d) When the insurance policy has been concluded and there is an agreement with the policyholder on periodic premium payment under the insurance policy, the insurer/ foreign non-life insurer’s branch shall record into its revenue the premiums already incurred in the respective premium payment period(s) and shall not record into its revenue the periodic premiums not yet incurred by the policyholder as agreed in the insurance policy.”.

Article 11. Adding Article 41a after Article 41 as follows:

“Article 41a. Expenses for support payments and remuneration payments for employees or members of socio-political organizations, socio-professional organizations, and cooperatives

1. An insurer/ foreign non-life insurer’s branch shall provide expenses for support payments and remuneration payments for employees or members of socio-political organizations, socio-professional organizations, cooperatives authorized by the insurer/ foreign non-life insurer’s branch to advise and arrange the conclusion of microinsurance contracts for the members of such organization after they have provided services to the insurer/ foreign non-life insurer.

2. An insurer/foreign non-life insurer’s branch shall, pursuant to Clause 3 of this Article and its specific conditions and characteristics, develop its own regulations on support payments and remuneration payments which must be consistently and publicly applied within the respective insurer/ foreign non-life insurer’s branch.

3. The maximum rate of support payments and remuneration payments payable, calculated on the bone fide premiums collected under each policy, by an insurer/ foreign non-life insurer’s branch to employees or members of socio-political organizations, socio-professional organizations, and cooperatives shall not exceed 5% of the maximum insurance agent commission rate corresponding to each policy under each type of non-life insurance, life insurance, or health insurance as prescribed in Clause 3 Article 51 of this Circular.”.

Article 12. Repealing Clause 3 and amending and supplementing a number of points and clauses of Article 42 as follows:

1. To amend and supplement Point e Clause 1 as follows:

“e) The Appointed Actuary must undertake that transactions related to various sources and types of insurance shall be aggregated and allocated to each source and type of insurance in a fair, reasonable, and consistent basis. At the end of year, the Appointed Actuary shall re-adjust the allocation of transactions related to the sources or types of insurance in accordance with this Circular, and in conformity with the principles notified to the Ministry of Finance, and the actual situation of the insurer.”.

2. To amend and supplement Clause 2 as follows:

“2. The At-law Representative, Appointed Actuary and Chief Accountant of the non-life insurer/health insurer/ reinsurer/ Vietnam-based foreign branch shall be responsible for establishing and registering the principles of revenue and expense allocation as specified in this Circular and notifying the Ministry of Finance and segregating the shareholders’ equity from the insurance premiums, as well as take accountability for the accuracy of data on the insurance premiums and the shareholders' equity. The Board of Directors or the Members' Council of the non-life insurer/ health insurer/ reinsurer, or the authorized body of the Vietnam-based foreign branch shall be responsible for approving the principles of revenue and expense allocation and supervising the implementation of such principles after they notify them to the Ministry of Finance.”.

Article 13. Amending and supplementing a number of points of Clause 43 as follows:

1. To amend and supplement Point a Clause 5 and to add Point a1 after Point a Clause 5 as follows:

“a) Insurance payouts less reinsurance recoveries, expenses for insurance technical reserving, expenses for insurance agent commissions, expenses for insurance brokerage commissions; bonuses and allowances and other incentives offered to insurance agents as agreed in the insurance agency agreements; initial training expenses and expenses for examination for grant of insurance agent certificates; expenses for knowledge improvement training for agents; expenses for recruitment of insurance agents; expenses for management of individual insurance agents; and expenses for inspection, supervision, and assessment of insurance agent quality;”;

a1) Support payments and expenses for remuneration payments for employees or members of socio-political organizations, socio-professional organizations, cooperatives authorized by the insurer/branch of foreign non-life insurer to advise and arrange the conclusion of microinsurance contracts for the members of such organization for the implementation of microinsurance;”.

2. To amend and supplement Point e Clause 5 as follows:

“e) General expenses, including administrative expenses and other expenses allocated to the insurance premiums according to the allocation principles notified to the Ministry of Finance;”.

3. To amend and supplement Point a Clause 6 as follows:

“a) General expenses, including administrative expenses and other expenses allocated to the shareholders' equity according to the allocation principles notified to the Ministry of Finance;”.

Article 14. Amending and supplementing Point b Clause 5, and to add Point b1 after Point b Clause 5 Article 46 as follows:

“b) Expenses for damage survey; bonuses and allowances and other incentives offered to insurance agents as agreed in the insurance agency agreements; expense for loss prevention/mitigation and expenses for risk assessment of the insured; initial training expenses and expenses for examination for grant of insurance agent certificates; expenses for knowledge improvement training for agents; expenses for recruitment of insurance agents; expenses for management of individual insurance agents; and expenses for inspection, supervision, and assessment of insurance agent quality;

b1) Support payments and expenses for remuneration payments for employees or members of socio-political organizations, socio-professional organizations, cooperatives authorized by the insurer/ branch of foreign non-life insurer to advise and arrange the conclusion of microinsurance contracts for the members of such organization or the implementation of microinsurance;”.

Article 15. Amending and supplementing Clause 5 Article 49 as follows:

“5. Information to be disclosed in a regular manner must be updated and accessible on the website of the insurer/ reinsurer/ Vietnam-based foreign branch.

With respect to the information to be disclosed in a regular manner specified at Point b Clause 2 Article 119 of the Law on Insurance Business, the insurer/foreign non-life insurer’s branch shall clearly specify the time limits for accepting or rejecting settlement of insurance claims and making of insurance payouts, and the handling of customers' opinions, requests, and complaints.”.

Article 16. Amending and supplementing a number of items of Clause 51 as follows:

1. To amend and supplement item a Point 3.2 Clause 3 Article 51 as follows:

“a) For individual life insurance policies:

Maximum commission rates applied to types of insurance are specified as follows:

- For insurance policies issued before July 01, 2024, the maximum agent commission rates are displayed in the following table:

Type of insurance | Maximum commission rate (%) | |||

Regular premium | Single premium | |||

First year | Second year | Subsequent years | ||

1. Term Life Insurance | 40 | 20 | 15 | 15 |

2. Pure Endowment insurance |

|

|

|

|

- With the term of 10 years or less | 15 | 10 | 5 | 5 |

- With the term of more than 10 years | 20 | 10 | 5 | 5 |

3. Endowment insurance: |

|

|

|

|

- With the term of 10 years or less | 25 | 7 | 5 | 5 |

- With the term of more than 10 years | 40 | 10 | 10 | 7 |

4. Whole Life insurance | 30 | 20 | 15 | 10 |

5. Annuity | 25 | 10 | 7 | 7 |

6. Universal life insurance |

|

|

|

|

- 10 years or less | 25 | 7 | 5 | 5 |

- More than 10 years | 40 | 10 | 10 | 7 |

7. Unit-linked insurance | 40 | 10 | 10 | 7 |

- For insurance policies issued from July 1, 2024 through December 31, 2026, the maximum agent commission rate is carried out as follows:

+ For insurance policies with the yearly renewable term of 1 year or less: 20%

+ For insurance policies with the term of more than 01 year:

Type of insurance | Maximum agent commission rate (%) | |||

Regular premium | Single premium | |||

First year | Second year | Subsequent years | ||

1. Term life insurance, whole life insurance | 40 | 20 | 15 | 15 |

2. Pure endowment, annuity, endowment insurance: |

|

|

|

|

- With the term of 10 years or less | 25 | 7 | 5 | 5 |

- With the term of more than 10 years | 30 | 20 | 10 | 7 |

3. Universal life insurance, Unit-linked insurance | 30 | 20 | 10 | 7 |

- For insurance policies issued from January 1, 2027, the maximum agent commission rate is carried out as follows:

+ For insurance policies with the yearly renewable term of 1 year or less: 20%

+ For insurance policies with the term of more than 01 year:

Type of insurance | Maximum agent commission rate (%) | |||

Regular premium | Single premium | |||

First year | Second year | Subsequent years | ||

1. Term life insurance, whole life insurance | 40 | 20 | 15 | 15 |

2. Pure endowment, annuity, endowment insurance: |

|

|

|

|

- With the term of 10 years or less | 25 | 7 | 5 | 5 |

- With the term of more than 10 years | 30 | 20 | 10 | 7 |

3. Universal life insurance, Unit-linked insurance (for the basic premium) | 30 | 20 | 10 | 7 |

+ The agent commission rate payable in respect of top-up premiums under universal life insurance policies and unit-linked insurance policies shall not exceed the percentage of premium load applicable to such top-up premium.

2. To amend and supplement item b Point 3.2 Clause 3 Article 51 as follows:

b) Maximum insurance agent commission rate for the basic premiums of pension policies: 3% of the total basic premiums;

The insurance agent commission rate payable in respect of top-up premiums under pension policies shall not exceed the percentage of premium load applicable to such top-up premium.”.

3. To amend and supplement item c Point 3.2 Clause 3 Article 51 as follows:

“c) For group life insurance policies: The maximum insurance agent commission rates shall be equal to 50% of the respective rates applied to individual life insurance policies of the same type of insurance specified at item a of this Point.”.

Article 17. Amending and supplementing a number of points of Clause 52 as follows:

1. To amend and supplement Point a Clause 1 as follows:

“a) For health insurance policies, term life insurance policies with the term of 01 year or less: The sum of bonuses, allowances and other incentives offered to agents shall not exceed 100% of insurance agent commissions of all health insurance policies, term life insurance policies in the fiscal year;”.

2. To amend and supplement Point a Clause 2 as follows:

“a) For agents conducting new business: The total bonuses, allowances and other incentives of agents in each fiscal year must not exceed the total 20% of the bone fide premiums collected under insurance policies with the term of 01 year or less and the yearly renewable term of 01 year, and 30% of the bone fide first-year insurance premiums collected under the regular premium payment mode or 7% of the bone fide insurance premiums collected under the single premium payment mode, for insurance policies with the term of over 01 year;”.

Article 18. Amending and supplementing a number of clauses of Article 53 as follows:

1. To add Point d after Point c Clause 3 as follows:

“d) Coordinating with the insurer/ foreign insurer's branch in supervising and inspecting to ensure the quality of insurance product introduction and advice activities carried out by the employees of the corporate agent; promptly coordinating with the insurer/ foreign insurer's branch in inspecting, reviewing, and handling policyholders' complaints relating to the advice provided by the employees of the corporate agent; and carrying out measures for handling violations (if any) in accordance with the decision of the insurer/ foreign insurer's branch.”.

2. To amend and supplement the title of Clause 4 and Point a Article 4 as follows:

“4. In case of distributing insurance products through any insurance agent, any insurer/foreign non-life insurer’s branch must:

a) Supervise and inspect to ensure the quality of insurance product introduction and advice activities carried out by the insurance agent; promptly inspect, review, and handle policyholders' complaints relating to the advice provided by the insurance agent. In case an insurance agent is found to have committed a violation, the insurer/ foreign non-life insurer's branch shall take measures to handle such violating insurance agent;”.

Article 19. Adding Article 53a after Article 53 as follows:

“Article 53a. Management of individual insurance agents

Management of individual insurance agents means an activity carried out directly by, or outsourced by, an insurer/ foreign non-life insurer's branch for the purpose of managing and supporting one or more groups of individual insurance agents in conducting the insurance agency activities prescribed in Clause 5 Article 4 of the Law on Insurance Business.”.

Article 20. Amending and supplementing Clause 2 Article 61 as follows:

“2. Within 30 days from the date of any change, the foreign insurer/ foreign reinsurer, or the foreign financial/insurance corporation, or the foreign insurance broker (in case of changing the head of the representative office) or the Vietnam-based foreign representative office (in case of changing the location of the Vietnam-based foreign representative office) must notify the Ministry of Finance. The notification dossier shall comprise:

a) A written notice, made using the form provided in Appendix XIII to this Circular;

b) The résumé, copy of the citizen identity card or the identity card, passport or another lawful personal identity paper as specified by law regulations, for the case of change of the head of the representative office. In case papers on the background and identity of Vietnamese citizens being part of the dossier as prescribed in this Circular have been integrated into the national database on population, the citizen identity database and other databases, the Ministry of Finance shall be responsible for exploiting and using information in the national database on population, the citizen identity database and other databases on the basis of information exchange and provision among state management agencies;

c) A copy of the lease agreement for the location of the Vietnam-based foreign representative office or evidence proving the right to use the location of the Vietnam-based foreign representative office certified by the representative office in case of relocating the Vietnam-based foreign representative office.”.

Article 21. Amending and supplementing Points a and b Clause 4 Article 62 as follows:

To replace the phrase “until the end of December 31, 2027” with the phrase “until the end of December 31, 2030” at Points a and b of Clause 4, Article 62.

Article 22. Replacing a number of appendices of Circular No. 67/2023/TT-BTC as follows:

1. To replace Appendix III, IV, X and XI with Appendix III, IV, X and XI issued together with this Circular.

2. To replace the reporting form No. 13-NT in Appendix VIII with the reporting form No. 13-NT in Appendix VIII issued together with this Circular.

Article 23. Effect

1. This Circular takes effect from July 2, 2026, except for the cases specified in Clause 2 Article 16 and Clause 2 Article 17 of this Circular, which take effect from January 1, 2027.

2. In case legal normative documents mentioned herein are amended, supplemented or replaced, these amending, supplementing or replacing documents shall apply.

3. Any problem arising in the course of implementation should be promptly reported to the Ministry of Finance for research and additional guidance.

Article 24. Transitional provision

The rate-making methodology and considerations or the technical reserving methods and considerations that have been approved by the Ministry of Finance before the effective date of this Circular shall continue to apply./.

| FOR THE MINISTER |

* All Appendices are not translated herein.

You are not logged in.

This feature is available to Advanced account holders. Please log in to access detailed information on Related documents.

If you do not have an account, please register here!

VIETNAMESE DOCUMENTS

This utility is available to subscribers only. Please log in to a subscriber account to download. Don’t have an account? Register here

This utility is available to subscribers only. Please log in to a subscriber account to download. Don’t have an account? Register here

ENGLISH DOCUMENTS

This utility is available to subscribers only. Please log in to a subscriber account to download. Don’t have an account? Register here

This utility is available to subscribers only. Please log in to a subscriber account to download. Don’t have an account? Register here